Merchant services billing can be confusing with many ways for processors to layer on additional charges. If you’ve looked at a merchant services statement and been unsure what exactly you’re paying for, you’re not alone.

Best Card, a CDA Endorsed Services partner, helps CDA members and their dental practices save money by regularly conducting cost analyses. Here’s what your practice should know about taking control of this often-overlooked expense.

Real costs versus made-up costs: An important distinction

Every time you accept a payment in the U.S., you pay a fee to process that transaction. Some of these fees are legitimate hard costs that every processor pays to the card brands. Others are flexible—or even entirely invented.

Real costs (paid by all processors on every transaction): These are the fees that go back to the banks and card brands. Some examples are:

- Interchange: The fee paid to the card issuer, determined by the type of card used and how the payment was accepted.

- Dues and assessments: Small fees paid to card networks like Visa and Mastercard to facilitate payments.

Negotiable costs (what most offices focus on when shopping processors): These include the pricing structures that processors offer along with recurring monthly fees like statement or Payment Card Industry fees. Some examples are:

- Flat rates

- Tiered rates

- Processor discount/fee earned

Made-up costs: These are fees that processors can quietly add to significantly boost their margins. Watch out for these fees:

- Transaction risk fees

- Risk assessment fees

- Settlement funding fees

- Non-EMV program fees

- Interchange surcharges

- Network security fees

- Technology fees

- Rate guarantee fees

Knowing the difference between each type of cost is the first step to protecting your bottom line.

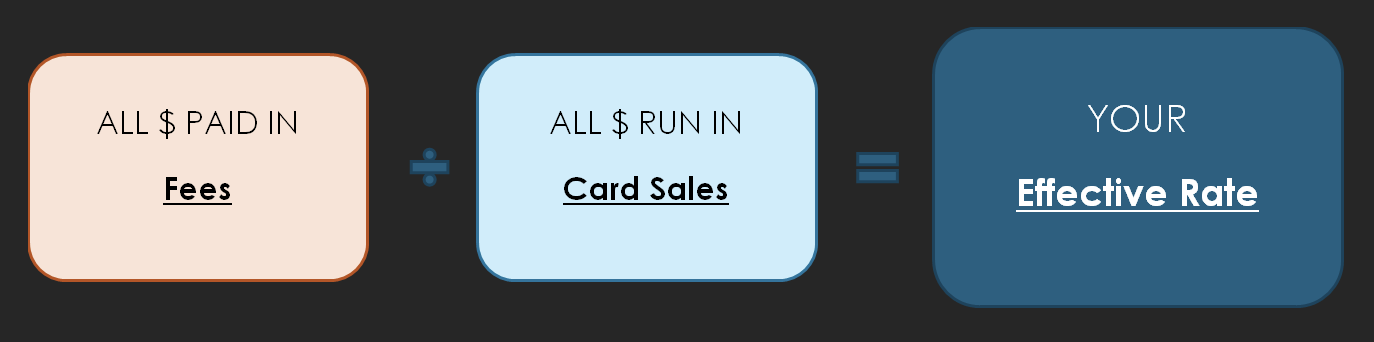

Not sure where to start? Calculate your effective rate

With so many fee types to track, a simple calculation can quickly tell you whether you’re being overcharged. Pull a recent monthly processing statement—or check your bank records—and use this formula:

What should your effective rate be?

The average CDA member’s dental office using Best Card paid an effective rate of 2.29% in 2025. By comparison, offices using competing processors paid an average of 3.56%—a significant gap that can add up fast.

Why do so many offices overpay?

- Many processors raise rates regularly, so a competitive deal six months ago may already be costing you more than you realize.

- It’s easy for processors to add “made-up” fees over time–offices often negotiate a low base rate but don’t notice new fees quietly appearing on statements.

- The most common mistake: choosing a processor primarily because it offers free equipment. Those “savings” typically get baked right back into higher monthly fees.

Interchange Plus: The pricing model to ask for

The more your fee structure mirrors the actual costs the card brands charge your processor, the lower your overall rate will be. Pricing models with one or two “flat” rates almost always cost more because processors need to build in a profit buffer to protect against variability in their own costs.

The solution? Ask for Interchange Plus pricing. This means you pay the direct passthrough costs, and the “plus” is a clear, fixed markup for the processor’s service. It’s the most transparent pricing model available and the easiest way to catch any unauthorized increases.

Exclusive CDA-member benefits with Best Card

Best Card offers all CDA members locked-in, guaranteed rates for the life of the member’s account with transparent pricing: Interchange Plus 0.30% + $0 per transaction, $100 off card readers and no cancellation fees.

On average, dental offices switching to Best Card save $6,795 (26%) per year and enjoy industry-leading customer service and payment technology that interfaces seamlessly with dental practice management software.

Ready to see what you could be saving? Complete and submit this brief form or call Best Card at 877.739.3952 for a detailed, no-obligation savings analysis.